I help founders understand their options clearly before they commit to any structure, provider, or direction.

For the disciplined investor, capital allocation begins not with opportunity, but with risk. Across UAE real estate markets, the separation between exceptional returns and capital impairment is most often defined by the rigour of the risk and due diligence framework applied. This document is not a guide to picking assets, but a foundation for building conviction. It outlines the structured thinking that professional investors, family offices, and long-term stewards of capital employ to preserve wealth and identify genuine value in a complex landscape. Here, risk management is your first duty and most significant competitive advantage.

Key Takeaways for the Strategic Investor

Real estate risk is multidimensional, extending beyond market prices to include illiquidity, developer solvency, operational costs, and regulatory shifts.

Due diligence is a continuous system of verification and analysis, not a pre-purchase checklist. It should encompass legal, financial, physical, and market realities.

Your investor profile—whether yield-focused, growth-oriented, or residency-driven—determines your specific risk exposures and required mitigations.

Institutional practices like position sizing, scenario stress-testing, and explicit liquidity planning are scalable disciplines for private investors.

Common investor failures often stem not from market downturns, but from controllable mistakes: over-leverage, inadequate exit planning, and misunderstanding total cost of ownership.

What "Investment Risk" Really Means in Real Estate

Unlike the near-instantaneous liquidity of public equities, risk in real estate is characterized by its illiquidity and operational tangibility. A stock portfolio can be rebalanced in seconds; a property investment is a long-term partnership with a physical asset, a specific location, a management entity, and a regulatory jurisdiction. The primary risk is a permanent loss of capital due to factors that could have been identified, assessed, and mitigated beforehand. In the UAE context, this is amplified by a market that attracts global capital flows, features distinct micro-markets, and operates within an evolving regulatory framework designed for stability and transparency. Thoughtful investing is less about timing the cycle perfectly and more about ensuring your capital is deployed in a resilient asset that can withstand cyclical pressures.

Core Categories of Real Estate Investment Risk

A professional framework requires disaggregating total risk into its core components. Each category demands its own analysis and mitigation strategy.

Developer & Counterparty Risk

This is often the foremost risk in off-plan purchasing and a significant factor in community management. It asks: Will the counterparty deliver on its promises? Beyond brand recognition, this involves scrutinizing financial health, construction track record, and corporate governance. Audits of developers can reveal risks in revenue recognition from off-plan sales, debt levels, and liquidity management. A project delayed by a year may not result in capital loss due to escrow protections but can incur substantial opportunity cost and disrupt residency or income plans. Understanding off-plan investment dynamics and developer assessment is essential for mitigating this category of risk.

Market & Cycle Risk

The UAE market is not monolithic. Oversupply in one community can coexist with scarcity in another. This risk involves misjudging the supply-demand dynamics of your specific sub-market and the broader economic cycle. Key drivers include global capital flows, oil price volatility, regional economic sentiment, and local job growth. While extreme boom-bust cycles have moderated due to stronger regulation, price consolidation and corrections remain features of a mature market.

Liquidity Risk

This is the risk of being unable to exit an investment promptly without conceding a material price discount. Liquidity varies dramatically by asset type, community maturity, and market phase. A studio apartment may rent easily but face a narrow resale buyer pool, while a premium villa may sell well but take longer to transact. In a downturn, this risk can magnify, making asset selection and holding period paramount.

Operational & Cost Risk

The ongoing cost of owning an asset can erode or negate projected returns. A frequent oversight is underestimating service charges, which in amenity-heavy or waterfront communities can be substantial. Other elements include maintenance costs, vacancy cycles, management fees, and the gap between projected and realistic rental yields once all expenses are accounted for. A property promising an 8% gross yield may deliver a 5-6% net return after all operational realities are factored in.

Financial & Leverage Risk

This encompasses loan structuring, interest rate exposure, and currency risk. With the AED pegged to the USD, UAE interest rates often follow U.S. Federal Reserve policy, affecting mortgage costs and market affordability. For foreign investors, currency fluctuations between their home currency and the AED can amplify gains or losses. Over-leverage remains a primary cause of investor distress, as it reduces cash flow resilience and can force sales at inopportune times.

Regulatory & Policy Risk

The UAE's regulatory environment is robust and increasingly sophisticated. Risks here stem from non-compliance or unanticipated changes. Key areas include evolving Anti-Money Laundering requirements requiring enhanced due diligence on fund sources, potential shifts in visa-linked investment thresholds, updates to building codes, and changes to ownership or inheritance frameworks. For instance, inheritance for non-Muslims typically defaults to Shariah law unless a specific will is in place. Regulatory frameworks are subject to change, and investors should maintain ongoing awareness of relevant updates.

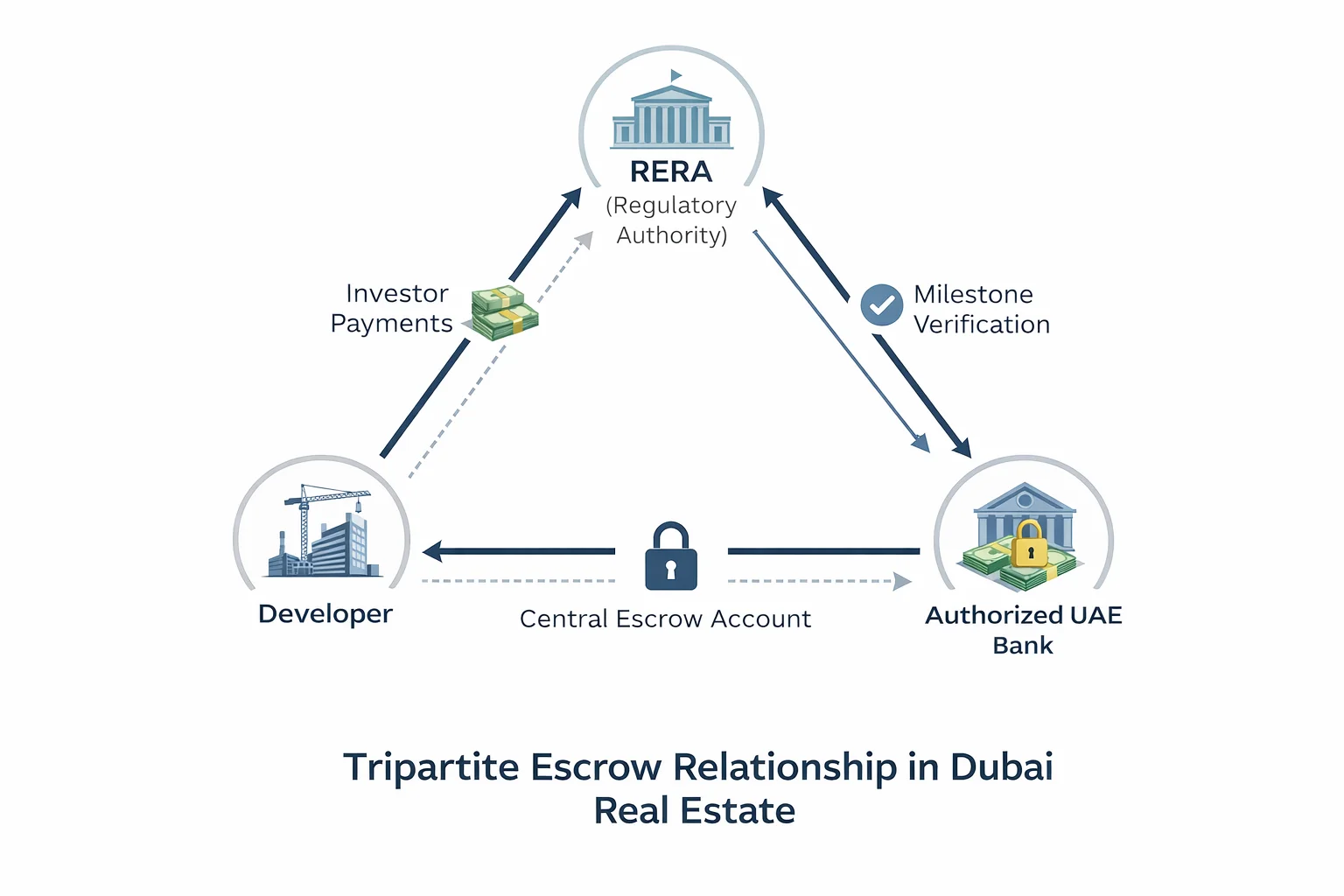

Escrow Account Verification for Investors

As part of comprehensive risk and due diligence, investors must verify the structure and compliance of escrow accounts used in Dubai’s off-plan market. A properly constituted escrow account, mandated under Dubai Law No. (8) of 2007 and overseen by RERA and the Dubai Land Department, serves as a statutory mechanism to segregate investor funds and link payments to verified construction progress.

Learn how to verify escrow compliance and understand both its protections and limitations.

Developer Financial Health: The First Line of Capital Protection

In off-plan and phased developments, the developer is your primary counterparty. Before assessing layouts, locations, or payment plans, disciplined investors evaluate whether the developer has the financial capacity, governance discipline, and execution strength to deliver the project through market cycles.

This includes reviewing delivery history, construction pipeline size, escrow compliance, funding structure, and warning signals that are often missed during aggressive launch phases. Escrow protects the process — not the outcome — making developer financial assessment a non-negotiable component of due diligence.

→ Read the Developer Financial Health Assessment Guide

Due Diligence as a System, Not a Checklist

For professionals, due diligence is a holistic, iterative process of validation. It transforms marketing claims into verified facts.

Pre-Purchase Evaluation & Strategic Fit

This begins with a clear alignment of the asset to your investment thesis. Is this a yield play, a growth bet, or a residency-driven purchase? Analyze the sub-market's supply pipeline, demand drivers, and economic fundamentals. An area with a proven track record and constrained supply typically carries different risks than an emerging district with substantial future inventory.

Legal & Structural Verification

Engage independent legal counsel to conduct definitive checks. This should include:

Title Deed Verification: Confirming freehold or leasehold status and clean title.

Encumbrance Check: Ensuring no mortgages, liens, or other claims exist on the property.

Developer & Project Viability: For off-plan, verifying RERA registration, escrow account status, and audit rights. The developer's escrow compliance is a critical safeguard.

Contract Scrutiny: Reviewing the Sale and Purchase Agreement for delivery timelines, penalty clauses, and defect liability periods.

Financial & Physical Audit

Financial Modeling: Build a detailed model incorporating all costs: purchase price, DLD fees (typically around 4%), agency commission, service charges, maintenance reserves, and financing costs. Stress-test the model against vacancy increases, rental declines, and interest rate hikes.

Physical Due Diligence: For ready properties, a professional structural survey is strongly recommended. It assesses the building's condition, systems, and identifies latent defects. For off-plan, review the quality of the developer's completed projects.

Exit Feasibility Thinking

Before buying, model the sale. Who is the likely future buyer? What is the historical liquidity profile of similar assets in this community? What alternative exit strategies exist? A clear exit hypothesis should be part of the initial thesis.

Aligning Risk with Your Investor Profile

Have questions about this?

A 10-minute call with Mirza often saves weeks of research. No obligation — ask anything about your situation.

Risk is not absolute; it is relative to your objectives, capital structure, and timeline.

| Investor Profile | Primary Objective | Highest Risk Exposures | Critical Due Diligence Focus |

|---|---|---|---|

| Yield Investor | Stable, predictable cash flow | Operational cost risk, tenant default risk, interest rate risk | Net yield calculation after all costs; rental market depth & tenant quality; lease structure |

| Growth Investor | Capital appreciation over 5-10+ years | Market cycle risk, liquidity risk, developer/brand risk | Supply pipeline analysis; community development trajectory; developer's brand equity and quality |

| Residency-Focused Buyer | Visa eligibility & lifestyle | Regulatory risk, developer delay risk, operational cost risk | Current visa regulations and mortgage impact; developer's on-time delivery record; service charge certainty |

| Business Owner / Family Office | Capital preservation, portfolio diversification, legacy planning | Concentrated position risk, regulatory complexity, succession risk | Portfolio position sizing; ownership structure; estate planning; holistic tax implications |

How Institutional Investors Manage Risk: Scalable Disciplines

Institutions manage risk through process and structure, not intuition. Private investors can adopt these scaled-down disciplines:

Position Sizing: No single property investment should compromise your overall financial stability. Determine in advance what percentage of your liquid net worth is appropriate for allocation to this illiquid asset class.

Diversification: Where possible, diversify across sub-markets and asset types, or consider real estate exposure via REITs for liquidity.

Scenario Analysis & Stress Testing: Model your investment under a "stress case" scenario. Could you sustain the cash flow? This reveals the true margin of safety.

Explicit Liquidity Planning: Maintain a dedicated liquidity reserve outside the property investment to cover expenses, vacancies, and emergencies without forced selling.

Continuous Monitoring: Treat due diligence as ongoing. Monitor regulatory announcements, community master plan updates, and the developer's financial health periodically.

Common Risk Mistakes Investors Make

The most painful losses are often self-inflicted. Avoid these critical errors:

Trusting Marketing as Analysis: Project brochures and promotional yield figures are starting points, not conclusions. Independent verification of all claims is essential.

Underestimating Total Cost of Ownership: Failing to factor in service charges, maintenance, agency fees, and potential refurbishment costs can lead to a significant gap between expected and actual returns.

Having No Clear Exit Plan: Buying without a hypothesis for selling is speculation. Understand the liquidity profile of your asset.

Over-Leveraging: Using maximum available debt removes your margin for error and can turn a manageable market dip into a solvency crisis.

Ignoring Regulatory Compliance: Assuming processes will be handled by others without your oversight. From AML source-of-funds checks to inheritance planning, regulatory compliance requires the investor's active attention.

Practical Investor Checklist

Use this structured checklist before committing capital.

Strategic & Market Due Diligence

- Clearly defined investment thesis aligned with the asset

- Analysis of community-level supply pipeline and demand drivers

- Verification of future infrastructure projects and master plan credibility

Legal & Regulatory Due Diligence

- Title deed and encumbrance report verified by independent lawyer

- For off-plan: RERA project registration & escrow account verification

- Review of all contract clauses, including delay penalties and defect liability

- Confirmation of visa eligibility rules if applicable

- Source-of-funds documentation prepared for AML compliance

Financial & Physical Due Diligence

- Detailed pro-forma model built, inclusive of all purchase and ongoing costs

- Model stress-tested for interest rate rises, rental decline, and vacancy

- For ready property: Professional structural inspection report reviewed

- For off-plan: Inspection of developer's past project quality

- Service charge history and future forecasts obtained and understood

Exit & Portfolio Review

- Exit strategy and target hold period documented

- Analysis of historical transaction liquidity for comparable assets

- Investment size reviewed as a percentage of total liquid net worth

Investor Notes

Service Charges: These are not optional. Obtain the official service charge schedule for the past 3 years and the projected budget for the coming year. In high-amenity buildings, they can exceed AED 25-40 per square foot annually, fundamentally altering net yield calculations.

The "Golden Visa" Detail: Investment thresholds and qualifying criteria are subject to regulatory frameworks that may evolve. When using financing, verification of how the investment value is calculated toward visa eligibility is advisable. Confirm the latest requirements with relevant authorities before contracting.

The Illiquidity Discount: In your financial model, consider applying an "illiquidity discount"—a required return premium over more liquid assets. This formalizes the compensation you require for locking up capital.

Who This Framework Is Most Relevant For

This framework is designed for investors who view real estate as a strategic component of a long-term capital allocation plan. It is particularly relevant for:

International Investors & Family Offices: Allocating capital to the UAE as part of a global portfolio diversification strategy.

Business Owners & Entrepreneurs: Seeking to build tangible asset bases, secure residency, and plan for legacy.

Long-Term Expatriates: Transitioning from renting to owning, with an eye on stability and potential future returns.

High-Net-Worth Individuals: Moving beyond single-asset purchases to a structured, risk-aware property portfolio.

Next Steps: From Framework to Action

A framework provides the map; navigating the terrain requires experience and structured dialogue. For those who are aligning capital with the long-term dynamics of the UAE real estate market, the next step is a disciplined review of your specific circumstances against these principles.

We facilitate this through structured investment strategy sessions, focused on translating your objectives into a clear risk-adjusted capital allocation plan, or portfolio risk reviews designed to audit existing holdings against the core risk categories outlined herein. This is not a sales conversation; it is a strategic discussion focused on building conviction, identifying blind spots, and ensuring your capital is deployed with clarity and discipline.

Request a Consultation

You may request a consultation to discuss your specific investment framework needs.

Advisory Disclaimer

This document is for informational and educational purposes only. It does not constitute financial, legal, or investment advice, nor does it constitute an offer to buy or sell any real estate asset. All real estate investment carries risk, including the potential loss of capital. The UAE regulatory environment is dynamic; all investors must conduct their own independent due diligence and seek counsel from licensed, independent legal, financial, and tax advisors before making any investment decision. Past performance of any market or asset is not indicative of future results.

Sources and official references

Official UAE bodies that govern the securities, banking, real-estate and investment matters discussed on this page:

- Dubai Land Department (DLD) - oversees escrow accounts (Dubai Law No. 8 of 2007), RERA project registration and real-estate transaction data

- Central Bank of the UAE - mortgage lending and interest rates, which track US Federal Reserve policy under the AED-USD peg

- Securities and Commodities Authority (SCA) - regulates funds and securities, relevant to REIT and diversified investment exposure

- UAE Government Portal - investing and doing business in the UAE, including Golden Visa and residency-linked investment rules

Ready to take action?

Whether you're ready to start or still comparing options — we'll give you a straight answer.

Chat on WhatsApp

Usually replies within 2h

Get a Free Quote

Personalised in 60 seconds

Call Directly

Sat–Thu, 9am–7pm UAE

About the Author

Dubai-based independent advisor on UAE visa, immigration, and offshore structuring. Founder of Henry Club UAE with 90+ published guides. Advisory-first — clarity before commitment.